Soaring Mortgage Rates Are Going To Make It Far More Difficult To Buy Or Sell A House

Did

you actually think that mortgage rates were going to stay at all-time

lows forever? Federal Reserve Chairman Ben Bernanke was able to grossly

distort the market for a while by buying up massive amounts of

government bonds and mortgage-backed securities, but there was no way in

the world that the market was going to stay that distorted forever. It

simply does not make sense to give American families 30 year mortgages

at a fixed interest rate of less than four percent when the real rate of

inflation is somewhere around eight to ten percent and the mortgage

delinquency rate in the United States is 9.72 percent.

If we actually did have "free markets" and they were behaving

rationally, mortgage rates would be far, far higher. Well, now that the

Fed has indicated that they are going to be starting to "taper" QE at

some point, bond yields have skyrocketed

and this is rapidly pushing up mortgage rates. According to Freddie

Mac, we just witnessed the largest weekly increase in mortgage rates in

26 years. Sadly, this is only just the beginning. Unless the Federal

Reserve intervenes, mortgage rates are going to continue to try to

revert to normal.

Did

you actually think that mortgage rates were going to stay at all-time

lows forever? Federal Reserve Chairman Ben Bernanke was able to grossly

distort the market for a while by buying up massive amounts of

government bonds and mortgage-backed securities, but there was no way in

the world that the market was going to stay that distorted forever. It

simply does not make sense to give American families 30 year mortgages

at a fixed interest rate of less than four percent when the real rate of

inflation is somewhere around eight to ten percent and the mortgage

delinquency rate in the United States is 9.72 percent.

If we actually did have "free markets" and they were behaving

rationally, mortgage rates would be far, far higher. Well, now that the

Fed has indicated that they are going to be starting to "taper" QE at

some point, bond yields have skyrocketed

and this is rapidly pushing up mortgage rates. According to Freddie

Mac, we just witnessed the largest weekly increase in mortgage rates in

26 years. Sadly, this is only just the beginning. Unless the Federal

Reserve intervenes, mortgage rates are going to continue to try to

revert to normal.When mortgage rates go up, so do monthly payments. All of a sudden, families that could afford the monthly payments on a $300,000 mortgage are no longer able to do so. This is why when mortgage rates rise, it tends to push housing prices down.

If rates continue to go up, it is going to become increasingly difficult to sell your house. Less people will be able to afford the monthly payments as rates rise. Many families will have to end up reducing their selling prices.

And right now we are watching rates rise at a rate that we have not seen since the 1980s. According to Freddie Mac, the average rate of interest on a 30 year fixed-rate mortgage jumped by more than half a percentage point just last week...

The average 30-year fixed-rate mortgage rose from 3.93 percent last week to 4.46 percent this week; the highest it has been since the week of July 28, 2011. This represents the largest weekly increase for the 30-year fixed since the week ended April 17, 1987.A year ago, the 30 year rate was sitting at 3.66 percent.

The monthly payment on a $300,000 mortgage at that rate would be $1374.07.

Currently, the 30 year rate is sitting at 4.46 percent.

The monthly payment on a $300,000 mortgage at that rate would be $1512.93.

If the 30 year rate rises to 7 percent, the monthly payment on a $300,000 mortgage would be $1995.91.

Does 7 percent sound crazy to you?

It shouldn't.

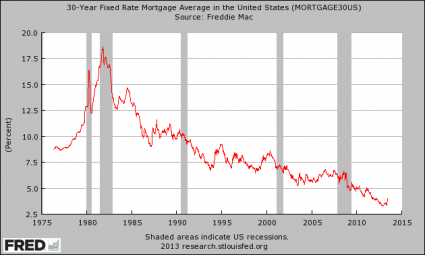

As the chart posted below demonstrates, a 7 percent mortgage was considered "normal" a decade ago...

As you can see, mortgage rates have nowhere to go but up.

And as they go up, they are going to absolutely crush any semblance of a "housing recovery".

Meanwhile, Americans continue to get poorer.

This week we learned that real per capita disposable income plunged at an annualized rate of 9.21 percent in the first quarter of 2013.

That is absolutely astounding. We haven't seen anything like that since the darkest days of the last recession.

If Americans do not have money to spend, that is going to hurt every industry - including housing.

And already we are seeing pain in the housing market. For example, the number of mortgage applications has fallen by 29 percent over the last eight weeks.

And rising rates are also causing a lot of families to turn to adjustable rate mortgages.

Remember those?

They played a major role in the last housing crash, and according to CNBC they are now making a comeback...

After hovering around record lows for the past few years, mortgage rates are rising dramatically. That has consumers not only shopping more but also considering adjustable rate mortgages, which offer lower rates and lower monthly payments.So what does all of this mean?

These ARMs, many requiring interest payments only, were popular during the latest housing boom but quickly fell out of favor when safer, fixed-rate loan rates fell to record lows.

It means that the tiny little "mini-bubble" that we have seen in housing this year is rapidly coming to an end.

It also means that it is going to become far more difficult to buy or sell a house. Monthly payments are going to go up substantially, and many homeowners are going to find that they are not going to be able to sell their homes for what they had anticipated.

If you are already in the process of buying a house, hopefully you locked in a really good rate while you could. Those record low mortgage rates sure were nice, and we will probably never see them again.

Now we are headed for a very painful "adjustment" thanks to Ben Bernanke and the Federal Reserve. They should never have distorted the housing market so much, and now we are all going to suffer the consequences.

No comments:

Post a Comment